Professional investors are increasingly interested in including real assets such as electricity, gas and water infra, toll roads, energy networks and airports. Global Listed Infrastructure Organisation (GLIO) is doing excellent work to raise investor awareness for these asset classes. Listed infrastructure has a lot in common with listed real estate, not least the importance of the spatial dimension and the capital intensity. Our alternative data offers a valuable additional perspective on these crucial assets.

140 European airport assets from six listed airport companies

We added circa 140 airport assets to our platform last month. These assets are owned by six listed Airport companies: AENA (Italy), Fraport, Tav Havalimanlari (Turkey), ENAV (Spain), Groupe ADP (France) and Zurich Airport. Assets include airports in various European countries from the Mediterranean to Great Britain and the east of Europe. Non-European assets are currently out of scope. This is particularly relevant for Zurich.

The 140 airport assets are added to our existing asset database of all major European REITs with professional disclosure. We have now added all our dimensions of spatial alternative data to these airports. This blog gives an insight into differences, similarities, and other interesting facts.

| Name | Country of Listing | # countries | # assets | Total Score (1-6) | Infra Score (1-6) | Weighting |

|---|---|---|---|---|---|---|

| ADP | France | 4 | 18 | 4.5 | 4.4 | Subjective |

| AENA | Spain | 2 | 50 | 3.1 | 3.7 | # Passengers |

| ENAV | Italy | 1 | 45 | 3.7 | 3.1 | Equal |

| Fraport | Germany | 4 | 18 | 2.5 | 2.0 | # Passengers |

| TAV | Turkey | 4 | 10 | 2.8 | 2.4 | # Passengers |

| Zürich AG | Switzerland | 1 | 1 | 5.0 | 4.7 | # Passengers |

Business models of listed airports vary widely, not least concerning ownership of the land and real estate. Investors should take a number of things into account when reading the company scores, as they are weighted scores of all airports in the portfolio. Fraport scores the (passenger weighted) lowest in infrastructure, with 2.0, as it has multiple assets on Greek islands, where infrastructure tends to be less efficient and sophisticated. ADP scores highest on infra as it is centred around Paris and major cities in Turkey and Zagreb, where the infrastructure is adjusted to the size of the inhabitants. The other Airport companies have mixed portfolios with both major cities and rural areas, decreasing their overall score.

The weighing of the asset share in the portfolios occurred according to the availability of data per company. As the small airports of ADP have no disclosure of revenues or the number of passengers, the assets are weighted on subjective economic importance. As a result Charles de Gaulle, Paris-Orly and the share in the Turkish airports are weighted the heaviest, while the rural airports are given lower weights. ENAV operates the control towers and Area Control Centres, hence has no distribution of revenue or passengers per asset. Therefore, all the assets are given equal weight in the portfolio. We were able to obtain more extensive data on the other listed airports. The number of passengers was chosen, since it is a better indicator than revenues.

ENAV and AENA strongly focus on their home countries, obtaining large landbanks and thus strengthening their influence and competitive advantage on future possibilities. Next to possibilities in aviation, current developments in sustainability and reducing carbon footprint might give way to other opportunities. As flying to destinations may become less popular, the current airport locations can shift their focus to new real estate development. Although the residential sector would be less interesting in these locations, feasible options include logistic development. Especially those places near large cities, where demand for new storage and distribution space is high.

The political dimension seems to be more important for airport assets than for conventional real estate. TAV Havilimanlari has acquired its airports in Eastern Europe, whereas Groupe ADP also has a minority stake in Schiphol Airport of 8% and has surrounding small airports in France. The national and international distributions of all assets can be seen in the map below, from the KR&A platform.

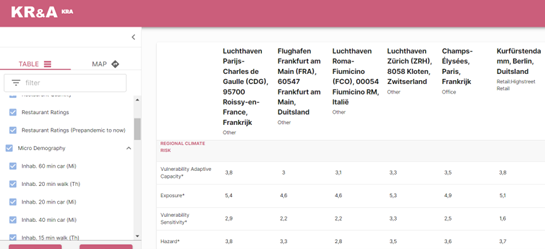

Our Flash Due Diligence gives insights into various aspects including NUTS3 data, micro-location data and climate data, as shown below. The analysed assets are the major airports of ADP, Fraport, ENAV and Zürich compared to two important real estate locations in central Paris and Berlin.

Interestingly, Zürich and Fiumicino airports are clearly further away from the city centre and other towns than Frankfurt and Charles de Gaulle are. The latter is more in line with the numbers reported by the two real estate hot spots. This has implications for future development, but also for alternative uses as described above. While Frankfurt and Charles de Gaulle may be harder to expand as they lie closer to dense areas, their potential for redevelopment may be higher, precisely because of their location.

Perhaps unsurprisingly, the overall score for the NUTS3 area is the lowest for Rome. The region is afflicted by lower quality of education, consumer income & wealth and demography compared to the other regions. The scores are 4.0, 2.8 and 3.2 consecutively. Particularly remarkable is the difference between the next best scores which are 4.8, 3.4 and 4.2 respectively. Comparing the real estate hot spots, they do not differ greatly in their scores even though Berlin scores significantly higher in demography while it stays somewhat behind in terms of infrastructure and the labour market.

Zooming in on the demography per sub-portfolio, airport companies* investing in East European airports will see a drastic decrease in population in the coming 10 to 20 years, whereas countries such as Germany, France and Switzerland are expected to see an increase. The impact of an ageing population will be mostly felt by AENA, ENAV and Fraport, as the majority of the population in their portfolio is 40 years or older. Nevertheless, the population projections for the invested countries are still positive, due to high immigration expectations. France and Germany have relatively young populations with a high concentration in the 0-19 or 20-39 categories. They too will likely see more immigration, while eastern European countries suffer both from high death rates and negative migration rates.

In conclusion, the introduction of airport assets marks the start of a new chapter for KR&A, from fairly strict real estate focus to the real asset industry. Geovisualisation made clear that many firms focus on countries close to their home country, where politics might be of great influence. Turbulent times in the aviation industry in terms of sustainability and reducing our carbon footprint add to the equation.

However, some assets might still have high potential regardless of the unpredictable future. These assets have beneficial locations for redevelopment into much sought-after real estate sectors. Furthermore, both micro and macro-demographics play an important role in expected returns for the six aviation companies. Assets far away from the city center are easier to expand, but often less attractive for redevelopment. The macro-demographics revealed that greying population can be offset by possible migration or can worsen it. Three major airports have similar characteristics based on their NUTS3 scores, although individual scores can vary greatly from overall scores and can still differ significantly from real estate hotspots. With our Flash Due Diligence, investors in this space can compare addresses and real asset companies with each other based on micro-locations attributes, NUTS3 areas, and on climate risk, gentrification, new property supply pipelines and on a country-scale.