A Compass for the Automated age

In the first blog we explored several themes, arguing for more human intelligence, pi-shaped people, and governance and oversight of AI-driven AVM models. In the blog I alluded to a lack of redundancy systems, which is a concern given the ratio of real estate debt relative to a country’s GDP. We questioned the merit of applying AVMs using unsensitized pricing data, resulting in likely skewed output. In this blog I want to challenge the notion of valuation as IRR-driven decision-making. An argument will be put forward that other investment criteria could be more prudent, specifically the role of better available hyper-local data and changes in the technology landscape that should drive investment decisions.

A broad range of outcomes

There is a common public consensus that a valuation must be spot on, akin to a dart landing in the bull’s-eye. Like a chess tournament between two grandmasters, take two of the best valuers in the world and it is plausible, and fair game, that their valuations can differ by ten percent. In absolute terms this is a twenty percent spread. This is an open secret and considered reasonable within the industry. The cause of these differences lies in the critical assumptions that are the foundation of a valuation. In a valuation report these are clearly laid out to the reader, whereas an AVM takes a different approach. An AVM steamrolls these assumptions, and likely a user of such a product is not even aware of the neglected assumptions and argumentation. Given the large variation in valuation, resulting in systematic risk to society, there should be recourse to a different investment approach. A valuation is often seen as an endgame, being the value itself, while the report contains much more insight on the location.

It is famously said, “valuation is an art, not a science.” The art refers to the core of a valuation report, which is the market analysis and highest and best use. The crux is having a feeling, or rather an understanding, of the property location. Thereafter the assumptions roll out.

Stabilized versus Market Values

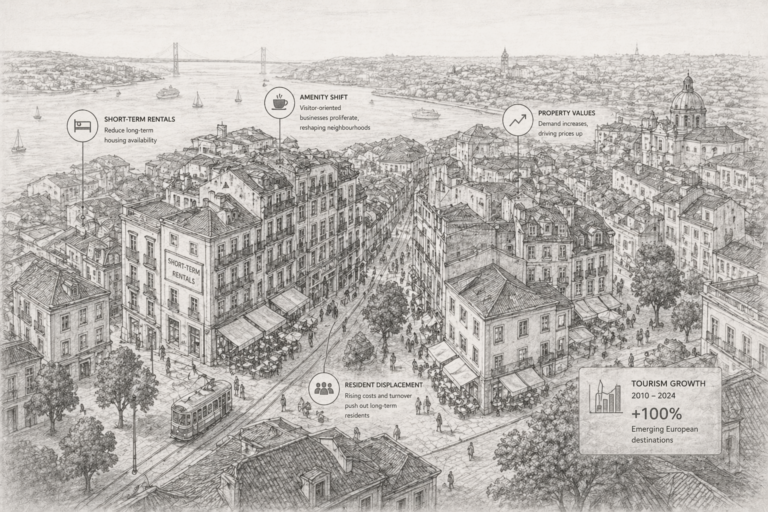

There exist different approaches to how value can be attributed. Market value is perhaps best-known concept, but investors could be better served with the concept stabilized value for their investment decision. A stabilized value is an interesting concept. Rather than valuing a property as-is, or using current or market rent, a valuer looks at the value drivers that determine market rent and yields. A key ingredient in these value drivers is the location. There is a significant correlation between a location quality and stable income, whereas a moderate location is more often resulting in unstable income. The predictability of income is the precursor to the value of the property. Thus, as we all already know, any investment decision starts with the location. But how to quantify that location?

AI allows new approaches

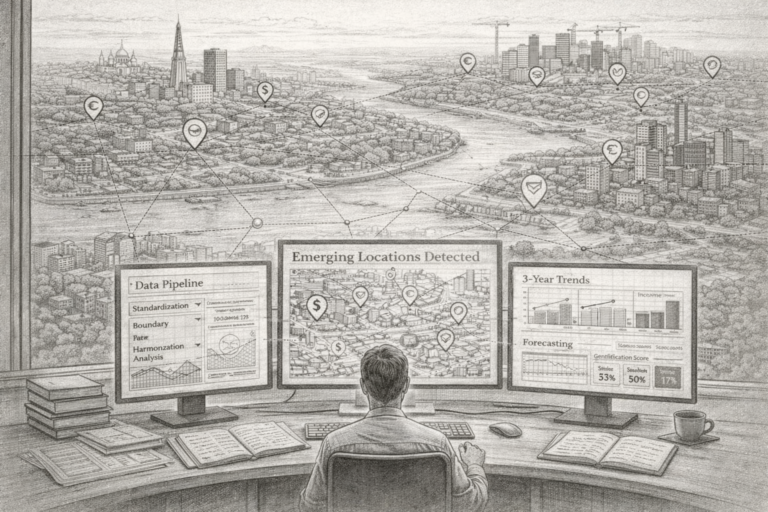

Measuring a location is the crux of any valuation report. A valuer will spend considerable time acquainting themselves with the neighbourhood dynamics, as can be read in two chapters in a valuation report, namely the property location and the market report. This time-tested luddite approach works well, but with big data, AVM models, and AI agents, investment managers could be better served by using that power to identify sites that will result in stabilized value.

Key ingredients of location data

The key ingredient is the classic combination of macro-economic data, demographics, market analysis, and the addition of hyper-local data. Samples of hyper-local data go to the microscopic level of restaurants, GPS signals, public transit movement, among others. These newly and readily available big-data variables provide previously unseen insights. A location insight can be calculated given the aforementioned variables at the local administrative unit (LAU) level. It is the hyper-local data that fine-tunes the lens in a microscope, giving sight of the location. These can then be cross-compared, giving a good indicator of the location’s worth. At this level a valuer or investment manager can compare and rank neighbourhoods from major cities across regions and countries. The question then becomes: at which sites should an entity be investing or leasing?

Conclusion

The concept is not new; it has been written eons ago, not in large language models but in actual long paragraphs. The age has come where big data is readily available, technology sufficiently powerful, and perhaps most relevant, mature enough to be relied upon. These new models use geographical systems that can pinpoint where stabilized values can be sought across large regions. Investment managers, portfolio managers, loan officers, and asset managers can learn a great deal by employing these new location methods. The question is not at what value, but at what location a manager will get the most stable future income.

It is surreal that investment decisions are still often made in spreadsheets with the holy spirit of IRR. IRR is a great indicator, but only post site selection. It is the new era of hyper-local data, driven by new technologies, that will be used as a competitive advantage to scout for stabilized investment. Value remains crucial in any valuation and investment decision, but more weight should be given to understanding the location.

Sebastian Hulshoff is KR&A’s head of AVM and Real Asset Valuations.

He can be reached at sebastian@knibberesearch.com