How alternative data can help us understand the risks and rewards of residential investment.

75% of responding investors said they will “significantly increase” their investment into European residential over the coming five years according to a recent investor intentions survey [1].

Introduction

Investors are having to be smarter in identifying locations that meet the requirements of residential investing while limiting the impact of regulatory risk. In this blog-article we highlight the value of alternative data in analysing the strength of residential segments and markets.

Demand for European residential real estate looks set to remain elevated over the next five years according to surveys of investor intentions. Despite a softening in market conditions in the second half of 2022, and growing regulatory risks, investors are convinced by the supply-demand dynamics across Europe’s major urban areas. The broadening range and availability of investment product across property types is a further attraction, but also a challenge for investment managers.

KR&A recently won its second tender from the European Commission (EC) for real estate data scraping, engineering and index construction. The EC selected the consortium to create residential indices based on asking prices from websites. It demonstrates that the company is a credible partner for institutional investors in developing a deeper understanding of the markets they operate in.

The growing interest in residential property

Interest in residential investment real estate has grown considerably since the financial crisis which is confirmed by changes in the sector composition of the FTSE EPRA Nareit Europe index. On the eve of Lehman, just 3% of companies in the index classified as residential. By the end of 2021, the share was 24%.

Figure 1: Annual residential investment volumes, in billions of euros [2].

Investment demand has been driven by attractive fundamentals, including migration to Europe’s larger urban areas, urbanisation, lack of supply and the rising cost of housing for sale in the most sought after markets. Moreover, there is a growing range of investment options available to pension funds and insurers via debt and equity markets and through private and listed public markets.

The residential sector appeals because of its perceived defensive fundamentals. Investors in search of long-term income typically look to take advantage of structural imbalances in housing supply and demand. The growing European institutional investment market is an added attraction, despite housing gaining an increasingly politically sensitive dimension.

The living spectrum embraces student housing, co-living, multifamily, single-family rental and seniors housing. Equity investors have also shown greater interest in funding affordable housing due to its attractive risk and return characteristics and, more recently, because it gives access to assets that can meet the social goals of their shareholders and stakeholders. Broadly speaking, all segments benefit from the same trends, namely urbanisation, demographic change, growing mobility, and structural undersupply of dwellings and housing affordability challenges.

Figure 2: Residential segments according to age breakdown and focus [3].

The changes influencing demand for living urban household-structures

For some time, investors have sought alternatives to the traditional commercial real estate sectors of retail and office. Changes to the way people work and shop have led investors to look for alternative sources of secure long-term property income. Residential property is one area which is viewed as offering a diverse range of investment options.

Residential markets have had to adapt to transforming household structures, population dynamics and urbanisation. The shift of young people with higher education to major urban areas is a theme across developed economies globally. Europe, Asia and North America have seen millennials trading their suburban roots for an urban lifestyle. Clearly this trend was interrupted by COVID, but recent evidence suggests that pre-COVID migratory patterns are returning.

Much of the existing stock of European housing was designed in the 19th and 20th C for large families. Twenty-first century households are smaller, typically consisting of 1 to 2 persons. The chronic mismatch between supply (type of housing) and demand (household size) has increased, affecting households across the age spectrum. Investors see the opportunity in creating more one-bed units, as well as the provision of co-living and micro-living solutions for those residents who face affordability constraints but value convenience and community over dwelling size. In addition, ageing populations are poorly served by a stock of senior housing that is insufficient in numbers and quality. Equally the provision of care is often inadequate and differs across Europe.

Regulation:

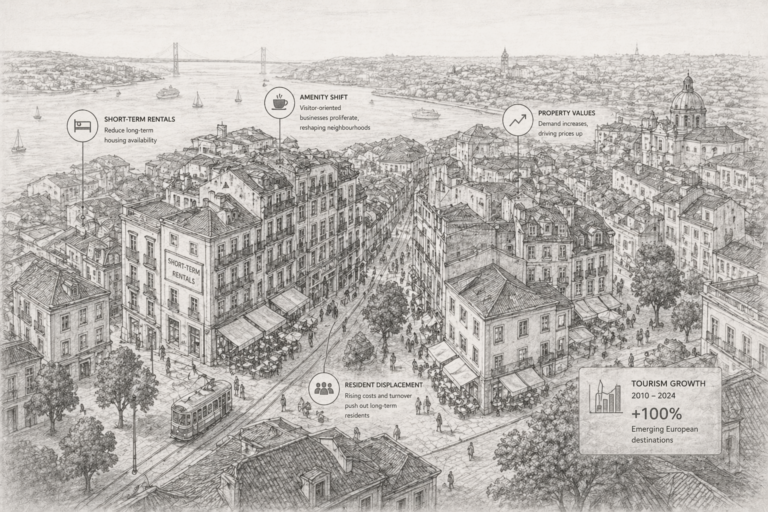

The impact of tightening regulatory regimes on residential performance is a consistent theme across the region. Residential has always been a highly regulated sector in Europe. A range of fiscal, planning and legal measures are used to control the housing market to meet desired political and socio-economic goals. Regulatory changes in the last decade, redefining market structures in many cities have added administrative complexity for landlords.

Concerns about housing shortages have prompted local and national governments to take steps to regulate the availability and affordability of dwellings. Market participants, therefore, need insights into taxation, legal systems, social governance and rent, lease and planning regulations. Furthermore, governments are starting to impose higher energy efficiency standards on residential buildings in line with their net zero ambitions.

The complex and dynamic regulatory landscape is prompting investors to look for diversification across markets and segments. Consequently, investors may combine segments like, senior and student housing with general needs rented residential to try and lower overall exposure to regulatory risk.

Figure 3: Rent regulation in Europe [4].

The analysis of three addresses in European Metropoles

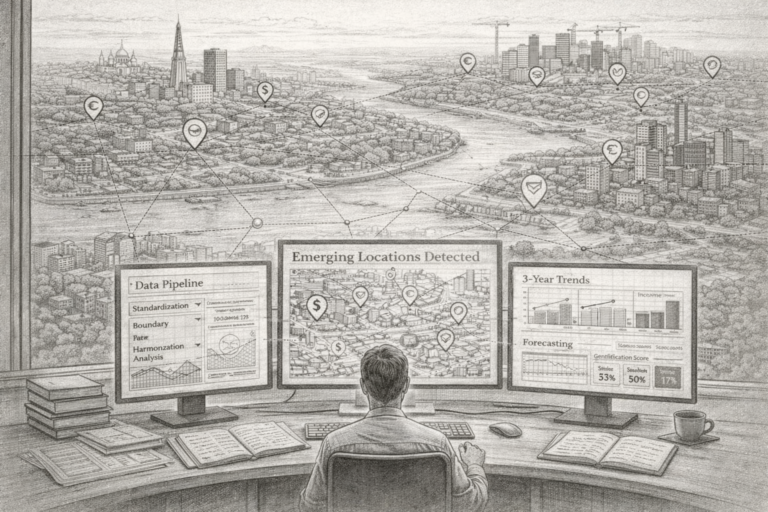

Investors can access a growing array of tools and datasets to make their investment decisions. Nonetheless, identifying the right region, city, local market and neighbourhood in the residential sector remains a complex process. Therefore, investors increasingly rely on alternative datasets and AI to augment their decision making process. The KR&A alternative data platform offers a tool that supplements traditional real estate top-down/bottom-up market analyses.

We looked at 3 well-known major city centre addresses, selected at random, to illustrate the type of alternative dataset we consider valuable in helping investors and landlords understand the market opportunities.

- 44, avenue des Champs-Élysées Paris,

- Kurfürstendamm 26a, Fasanenstraße 75, 10719 Berlin,

- Via Alberto Lionello, 201, 00139 Rome.

We highlighted in a previous blog the key variables that particularly influenced the performance of residential investment markets.

- The underlying demographics of a market and region;

- The strength of the overall economy;

- The health of the labour market;

- The state of consumer finances.

We also assessed markets across several localized amenity metrics and look at climate related metrics which could impact the perceptions of a location’s attractiveness.

Table 1: Normalised scores (1-6) of population growth and population density by region.

| Demography (national bucket) | Population | Population Growth 3Y | Population Projection 2020-2025 | Population Projection 2020-2030 | Population Projection % growth 2020-2025 | Population 0-19 | Population 20-39 | Density | |

|---|---|---|---|---|---|---|---|---|---|

| Berlin | 1.0 | 6.0 | 5.0 | 6.0 | 6.0 | 5.6 | 2.1 | 6.0 | 6.0 |

| Paris | 1.0 | 6.0 | 2.4 | 6.0 | 6.0 | 6.0 | 2.4 | 6.0 | 6.0 |

| Roma | 1.0 | 6.0 | 1.0 | 6.0 | 6.0 | 5.9 | 1.8 | 2.0 | 3.7 |

Source: KR&A December 2022

Population dynamics by age groups

The properties are in locations with varying population dynamics. While the youngest, dependent age group is relatively small in all 3 cities, both Paris and Berlin score highly in the age group crucial for multi-family demand, the 20-39 year olds. Overall population growth looks strong across Berlin, Paris and Roma, particularly in the age group likely to spur demand in the multi-family segment, and potentially student housing. Although amongst the youngest (0-19) age cohort, none of the cities stand out as being sources of potential local demand for student housing.

Clearly, migration data will have an important bearing on student property demand, particularly in the age cohort under 30. Both Berlin and Paris are relatively densely inhabited cities, again supporting the argument for considering them as destinations for residential investment.

Table 2: Normalised scores (1-6) of young population dynamics by region.

| Population age 0-19 | Population age 20-39 | Population Projection 2030 age 0-19 | Population Projection 2030 age 20-39 | Migratory Pop. change 2017-'50 | Change in Pop. density 2017-'50 | |

|---|---|---|---|---|---|---|

| Berlin | 2.1 | 6.0 | 5.1 | 5.1 | 1.0 | 1.0 |

| Paris | 2.4 | 6.0 | 6.0 | 4.8 | 6.0 | 6.0 |

| Roma | 1.8 | 2.0 | 1.2 | 3.1 | 1.0 | 1.0 |

Table 3: Normalised scores (1-6) of older population dynamics by region.

| Population age 60-79 | Population age >=80 yrs | Population Projection 2030 age >=80 yrs | Population Projection 2030 age 60-79 | |

|---|---|---|---|---|

| Berlin | 1.5 | 3.7 | 6.7 | 1.0 |

| Paris | 1.0 | 2.8 | 6.4 | 1.0 |

| Roma | 3.1 | 4.8 | 8.1 | 3.9 |

Source: KR&A December 2022

At the other end of the age spectrum, Italy has most promising demographics for senior housing, which is reflected in Roma’s 80+ population score and projections for this age cohort over the next decade. Naturally, an elderly population is not the only pre-requisite for market selection for senior housing and assisted living accommodation. For example, markets with strong economies, with inhabitants with access to relatively high disposable incomes and personal wealth will be more attractive for private pay health care.

The strength of the economy, labour markets and household wealth

All the addresses are in cities that are amongst Europe’s wealthier locations. They are attractive locations for businesses, economic migrants and therefore investors. The regional economies rank highly. Disposable incomes are relatively high, although individual consumer income and wealth are more modest compared to broader European markets.

The labour markets of Berlin and Paris are considerably stronger than Roma, with higher level of economically active persons and a broadly better educated workforce. Consequently, the strength of the economies of these cities appear to underpin the demographic reasons for considering the investment potential for multi-family or student accommodation

Table 4: Normalised scores (1-6) of disposable income and household wealth.

| Disp income of HH | Growth Disp income of HH | Consumer Income & Wealth | GDP/inh. | GDP/inh. as % of EU av. | GDP | PPS/inh as% of EU av. | |

|---|---|---|---|---|---|---|---|

| Berlin | 4.9 | 2.3 | 3.6 | 5.1 | 5.1 | 6.0 | 5.1 |

| Paris | 5.7 | 1.0 | 3.4 | 6.0 | 6.0 | 6.0 | 6.0 |

| Roma | 4.6 | 1.0 | 2.8 | 4.7 | 4.7 | 6.0 | 5.2 |

Table 5: Normalised scores (1-6) of labour market strength.

| Persons in Employment Activities | Employment (20-64y) | Employment (20-64y) change vs 2012 | TE of Active pop. | |

|---|---|---|---|---|

| Berlin | 5.4 | 4.6 | 2.9 | 5.4 |

| Paris | 6.0 | 4.5 | 2.4 | 6.0 |

| Roma | 4.4 | 1.5 | 1.4 | 2.2 |

Source: KR&A December 2022

Climate factors

Assessing climate risk has assumed greater importance in making long term investment decisions. Investors now need to analyse a range of environmental transition and physical risks that can materially impact their portfolios. The response by regulatory authorities to climate risk is influencing the regulatory framework affecting asset owners.

The KR&A alternative data platform can help investors assess climate risk alongside the socio-economic characteristics in each market. It offers regional climate risk predictions and micro-locational climate risk facts. The table below shows the relative risks from climate factors across the city regions the three properties are located in. None of the assets are in markets which are more exposed to extreme weather change than the European benchmark. The tool allows closer examination of markets which have a greater potential physical risk in the future. Or more likely, could face additional regulatory risk from governmental agencies aimed at addressing their perceived risk.

Thus, Roma appears to be vulnerable to the effects of rising temperatures across a range of metrics. In contrast, Paris is assessed as having a relative vulnerability to flooding and more likely to be exposed to the dangers, and cost of measures to mitigate the perception of the growing risk of fluvial flooding.

Table 6: Normalised scores (1-6) of climate projections per city.

| Projected change in very heavy precipitation days (RCP 8.5) | Drought hazard | Projected change in mean temperature (RCP 8.5) | Projected change in heat wave days (RCP 8.5) | Fluvial hazard | |

|---|---|---|---|---|---|

| Berlin | 3.5 | 2.9 | 4.3 | 5.4 | 1.0 |

| Paris | 3.5 | 4.6 | 5.2 | 4.9 | 1.0 |

| Roma | 3.5 | 1.0 | 2.7 | 1.0 | 4.4 |

Source: KR&A December 2022

Amenities

Undoubtedly the type of foregoing analysis is helpful in choosing a city. But then we need to assess the population densities and type of amenities a location offers to residents to make it attractive. As major capitals, these markets characteristically offer good rail and road transport links, especially Berlin and Paris, as well as international accessibility. As a proxy for wealth and gentrification of the three micro-locations, we look at the number and price range of nearby restaurants over time.

We also can look at the population within a short walking distance and the number of construction sites within a given radius. The properties in Paris and Berlin are in more densely populated locations which are more typical residential districts. Likewise, they are well served by amenities, particularly in Paris. At first glance, supply constraints seem to be more persistent nearby the Roman address than at the other two micro-locations, as illustrated by a comparison of the building site proximity.

Table 7: Amenities analyses per city.

| Inhab. 5 min walk (Th) | Inhab. 10 min walk (Th) | Inhab. 15 min walk (Th) | Building Sites <0.5 km | Building Sites <1 km | Gentrification Score - changes in price categories < 500m | Restaurants < 500m (number) | Restaurants < 500m (score) | Tot. Michelin Stars < 500m | |

|---|---|---|---|---|---|---|---|---|---|

| Avenue des Champs-Élysées 44 Paris | 5.5 | 19.6 | 44.7 | 6 | 6 | 1.2 | 385 | 6.0 | 6 |

| Kurfürstendamm 26a Berlin | 1.9 | 10.5 | 26.0 | 7 | 14 | 1.1 | 125 | 5.5 | 0 |

| Via Alberto Lionello 201 Roma Italy | 0.1 | 2.8 | 5.3 | 0 | 4 | 1.3 | 31 | 2.1 | 0 |

Source: KR&A December 2022

Sources

[1] European Living Sectors Investor Survey, Knight Frank, Q3 2022

[2] Knight Frank, MSCI, October 2022

[3] Savills IM, KR&A estimations, November 2022

[4] Hanna Kettunen, Hannu Ruonavaara, Rent regulation in 21st century Europe. Comparative perspectives. May-20. Journal of Housing Studies.